- We Study Markets

- Posts

- 🎙️ Bigger Not Better

🎙️ Bigger Not Better

[5 minutes to read] Plus: Stocks are more sensitive to rates

Shawn O'Malley & Matthew Gutierrez

July 03, 2024

By Matthew Gutierrez and Shawn O’Malley

Happy Fourth of July, everybody!

The S&P 500 and tech-heavy Nasdaq indexes are definitely celebrating after closing Wednesday at new all-time highs. The S&P is having its second-best start to an election year ever — only 1976 was better.

Yet as we’ve explored before, only one-fourth of stocks in the index have hit new highs this year. That continues the trend of 2023, when only 30% of stocks outperformed the benchmark.

What gives? Well, for starters, relatively few companies outside of the Magnificent 7 are seeing truly notable earnings momentum. Big Tech powered the 14.5% gain for the index, which was the 15th-best start to any year going back to 1928.

— Matthew & Shawn

Here’s today’s rundown:

Today, we'll discuss the biggest stories in markets:

The S&P 500 is more and more sensitive to rates

Why hedge funds are too big to beat the market

This, and more, in just 5 minutes to read.

POP QUIZ

Chart(s) of the Day

Sponsored Content

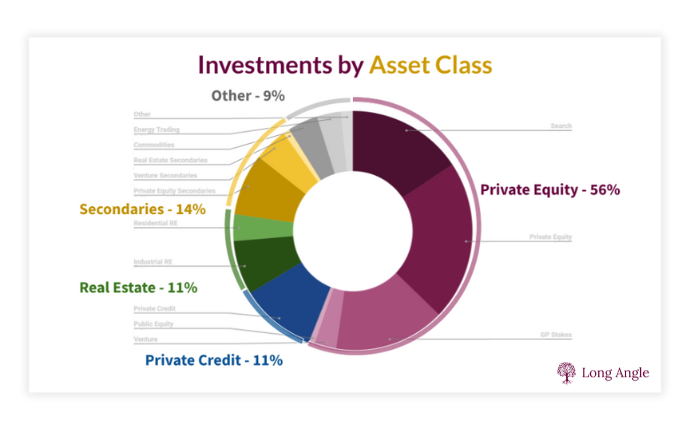

Private Markets, Powered by Collective Expertise of HNW Investors

Investing in private market opportunities is challenging. The difference between success and failure in private markets comes down to your network.

Long Angle is a vetted community of 3,000 high-net-worth investors who leverage their collective expertise and scale to access and underwrite some of the world’s best alternative asset investments.

After reviewing hundreds of opportunities, Long Angle diligence deal teams greenlight a dozen deals each year. Asset classes range from Private Equity, Search Funds, and Private Credit to Secondaries, Real Estate, and Venture.

No membership fees. All members receive equal access to negotiated fee discounts powered by the community’s $45 billion in collective assets.

In The News

🤔 Interest Rate Sensitivity Picks Up For the S&P 500

Giphy

The S&P 500 index keeps on changing, both in terms of composition and risk profile.

Consider that Goldman Sachs research found that equities leadership hasn’t been this narrow since the 1930s. The top five holdings in the S&P 500 now make up 27% of the index, the highest concentration we’ve seen with data since 1980.

The point: The index has evolved considerably over the past five decades, specifically in its components, interest-rate sensitivity, dividend yield, and volatility.

Dividends: The S&P 500's dividend yield has fallen from 4.11% in the 1970s to 1.45% in the 2020s. Dividends can lower the volatility of stocks for investors by mitigating losses.

Components: In the 1970s, industrials and materials constituted 26% of the S&P 500. Now? They account for only 10.6% of the index.

Meanwhile, the information technology and financial sectors have been on the rise — finance and big tech, basically. The two sectors combined made up just 13% of the index in the 1970s but have since become the dominant forces. They now comprise 42% of the index by weight.

Top heavy: The technology sector alone represents 29 percentage points of that 42% figure, a kind of concentration further emphasized by the fact that six out of the top seven positions in the S&P 500 by weight are currently tech companies. (Berkshire Hathaway and Eli Lily are the only non-tech companies in the top 10.)

Interest rate sensitivity: The index has become more sensitive to interest rates mostly because of its high concentration in tech and financial stocks. Take 2022, when the Federal Reserve raised rates by 5 percentage points, the S&P 500 declined by 20% for the year. Many tech stocks were hit much harder.

“Expectations for earnings growth are at a record high, and even a slight change in interest rates can derail valuations,” WSJ reported.

Many tech companies rely on future earnings potential rather than current profits. Higher interest rates make future earnings less valuable in present terms, hurting valuations. Plus, tech companies often require a lot of capital for research, development, and expansion, so higher interest rates increase borrowing costs, which tends to eat into profitability and growth prospects.

Global correlation: The correlation between the S&P 500 and the top 10 world stock market indexes — Germany, the U.K., France, South Korea, Hong Kong, Japan, Toronto, China, Mexico and Brazil — has increased drastically. Consider that in the 1970s, the average correlation was 0.24. By the early 2020s, this correlation had jumped to 0.70.

From The Wall Street Journal

Why it matters:

The shift is noteworthy and has key implications for investors. Notably, the increased exposure to tech and financial stocks has made the index more sensitive to interest rate fluctuations and more correlated with other global indexes, all of which impact its effectiveness as a diversification tool.

Because the S&P 500 isn’t all that diversified anymore, research also suggests that investors holding S&P 500 index funds are now exposed to risks similar to those associated with direct investments in tech firms. Risks include heightened sensitivity to interest rates, high price valuations, and expectations of substantial growth rates.

Stay diversified: The Wall Street Journal notes that the traditional 60-40 portfolio strategy may no longer provide the same level of diversification as it did in the past, and simply adding international stocks to a portfolio may not effectively reduce volatility because of greater global correlations.

Alternate assets: A professor of finance at George Mason University pointed out that investors seeking diversification benefits similar to those of the past may need to consider including commodities, alternative assets, and other weakly correlated asset classes in their portfolios.

That’s one of the reasons gold and bitcoin have become more popular over the past few years. And if the S&P 500 keeps becoming more tech-heavy, those alternatives could become even more attractive.

Read more on how rates impact stocks

More Headlines

🤠 Jeff Bezos to sell $5 billion of Amazon shares as stock hits new highs

💼 U.S. private payroll growth slows in June

😃 Powell encouraged by cooler inflation data

🌎 Why borderless talent is the future of work, per CEOs

📈 The case for more stock gains in the second half of 2024

😬 Citi was money launderers’ favorite bank

🚗 Tesla shares soar on better-than-expected deliveries report

📉 Hedge Funds Have Gotten too Big to Beat the Market

There are headlines out there like, “You Can Shred the Average Hedge Fund by Doing Basically Nothing.” It’s not clickbait — it’s the truth, as simple, low-cost S&P 500 index funds have been beating top hedge funds for years, despite all their Ivy League minds, mathematical models, chart skills, and long hours at the office.

Recall that in 2008, Warren Buffett famously placed a million-dollar bet that an S&P 500 index fund would beat the funds of funds hedge fund managers would select. Of course, the Oracle of Omaha was proven right.

On the decline: After a hot start in the 1990s, it’s been tough sledding for hedge funds. Once darlings of the investment universe, they’ve lost their luster.

Take Bobby Jain's new multi-strategy fund, Jain Global, which has raised $5.3 billion in commitments. Even though it’s one of the largest hedge fund launches ever, it has generated relatively little excitement.

Muted response: The reason for this muted response lies in the declining performance of hedge funds. After a strong start in the 1990s, hedge fund returns have consistently underperformed major benchmarks, and the industry has struggled to maintain its edge.

Why? Buffett has blamed arrogance, greed, and most investors’ short-term time horizon as the lead reasons, and he’s likely correct.

At capacity: A new Bloomberg analysis shows that the core issue appears to be capacity. The hedge fund industry has grown from tens of billions of dollars in the mid-1990s to a multi-trillion-dollar business a decade later. As of the end of 2023, North American hedge funds managed $3.7 trillion, up from $2.2 trillion in 2014. The numbers keep going up.

That growth has led to diminishing returns. The Credit Suisse Multi-Strategy Hedge Fund Index, which peaked at 10.7% annual returns during the decade ending in 2004, has since declined to just 5.2% per year over the 10 years through May.

In comparison, the S&P 500 Index has outperformed the multi-strategy index by 3.5 percentage points annually since 1994, including dividends. It has beaten hedge funds about two-thirds of the time over rolling 10-year periods.

Yet hedge funds continue to charge large fees (though fees are slowly coming down), typically more than 1% in annual management fees plus nearly 20% of profits.

Why it matters:

Hedge funds are trying to evolve. They’re promoting star stock pickers, emphasizing risk-adjusted returns, and, more recently, advocating for multi-strategy approaches. Yet performance has still lagged.

Thus, net flows to North American hedge funds have slowed considerably, amounting to just $4.6 billion since 2015 through last year, suggesting that while existing assets have grown because of rising asset prices, new money flowing into hedge funds has been limited.

Outlier: One notable exception to the industry trend is Renaissance Technologies' Medallion fund, widely regarded as the best-performing hedge fund of all time.

Perhaps one of its greatest strengths is its ability to recognize capacity constraints: Medallion limits its size to about $10 billion and regularly returns money to investors to maintain the cap.

Final thoughts: It remains to be seen how long investors will continue to allocate capital to funds that have struggled to do well, especially when accounting for their fees.

As Bloomberg’s analysis concludes, “A few hedge funds may continue to make a lot of money for a fortunate few. The industry can’t do better than that at its current size, no matter how much talent it hires. The only question is how long it will take investors to come to terms with it.”

Together With Hims

ED Treatment For Under $2 Per Day*

ED is a complicated issue that affects millions of men worldwide. Luckily, the solution is simple with Hims.

Hims offers access to personalized and affordable ED treatment. They’ve helped thousands of men like you and are on a mission to help the world feel great.

ED treatment has never been simpler.

The process is simple and 100% online. After completing an intake form, a licensed medical provider will review and determine if a prescription is appropriate. If prescribed, medication ships to you for free in discreet packaging.

Start your journey today.

*Actual price to customer will depend on product and subscription plan purchased. Prescription products require an online consultation with a healthcare provider who will determine if a prescription is appropriate. Restrictions apply. See website for full details and safety information.

Quick Poll

Do you currently hold an S&P 500 index fund in your portfolio? |

On Monday, we asked: Which of these AI uses for investing interests you most?

— Answers were evenly spread. Readers are interested in AI’s help with stock recommendations, general market insights, analyzing specific stock risks, and discovering new stock ideas to research.

— Said one reader: “There are no magic formulas out there. If there were, they would soon become obsolete. Common sense, patience and investing in what I understand, seem to work best for me.”

— Another said, “It can be a quick method of gathering some initial data on aspects of companies you are looking at. It can speed up the work you do to evaluate a company but cannot replace the fundamental work you need to do, hence I would never use AI for recommendations.”

TRIVIA ANSWER

See you next time!

That's it for today on We Study Markets!

Enjoy reading this newsletter? Forward it to a friend.

Was this newsletter forwarded to you? Sign up here.

Use the promo code STOCKS15 at checkout for 15% off our popular course “How To Get Started With Stocks.”

Advertise with us.

Follow us on Twitter.

Keep an eye on your inbox for our newsletters on weekdays around 6pm EST and on weekends. If you have any feedback for us, simply respond to this email.

You can also leave your comments/suggestions/feedback anonymously here.

What did you think of today's newsletter? |

All the best,

P.S. The Investor's Podcast Network is excited to launch a subreddit devoted to our fans in discussing financial markets, stock picks, questions for our hosts, and much more!

Join our subreddit r/TheInvestorsPodcast today!

© The Investor's Podcast Network content is for educational purposes only. The calculators, videos, recommendations, and general investment ideas are not to be actioned with real money. Contact a professional and certified financial advisor before making any financial decisions. No one at The Investor's Podcast Network are professional money managers or financial advisors. The Investor’s Podcast Network and parent companies that own The Investor’s Podcast Network are not responsible for financial decisions made from using the materials provided in this email or on the website.